If you own a US LLC, receive payments from US companies, sell products on platforms like Shopify, Amazon or Gumroad, or earn royalties, licensing fees, dividends, commissions, or any other type of income from a US source – there is a very high chance you will be required to fill out either a W8 or a W9 form at some point.

We have talked to hundreds of foreign entrepreneurs going through this exact moment – they are trying to get paid, a payer drops a W8 or W9 request on them, and suddenly a straightforward payment turns into a paperwork headache. For many foreign business owners, these forms feel confusing and intimidating.

They are IRS forms, after all, and no one wants to get their US tax obligations wrong. But in reality, once you clearly learn what these forms actually do and why they exist, filling them out is a much more manageable and smooth task.

This guide will walk you through everything you need to know about W8 and W9 forms – what they are, who needs to file which one, how to fill each one out step by step, and what special rules apply to US LLCs, foreign partnerships, and business owners claiming tax treaty benefits.

What Is Withholding Tax, and Why Does It Matter?

Before getting into the forms themselves, it helps to understand the concept of withholding tax, because W8 and W9 forms exist primarily to serve the US withholding tax system.

The United States operates one of the most comprehensive withholding tax regimes in the world. Nearly all types of US-connected income – a category the IRS refers to as Effectively Connected Income (ECI) – are subject to withholding tax. This includes income such as:

- Royalties

- Dividends

- Interest payments

- Rental income from US properties

- Payments for services performed in the US

- Sales proceeds from certain US assets

Withholding tax means that the tax is not paid by you directly to the IRS – instead, it is collected and remitted automatically by the payer. For example, if you are a UK-based developer selling a software tool to US customers through Gumroad, the e-commerce marketplace will calculate the US tax owed on your earnings, withhold that amount, and send it to the IRS on your behalf.

You receive the net amount after the tax has already been deducted from your earnings. The same thing happens when you are receiving contractor payments through Stripe or getting paid out by any other US-based platform like Amazon.

As you can see, this system has two major practical advantages. First, as a foreign business owner or non-US resident, it means you often do not need to file a full US tax return just to report that income – the tax has already been handled at the source. Second, it makes enforcement much easier for the IRS, because the legal responsibility for collecting and remitting the tax falls on the US-based payer, who is under US jurisdiction.

However, for this system to work perfectly, the payer needs to know who you are and what your tax status is – because the amount of tax to withhold can vary significantly depending on:

- Whether you are a US tax resident or a non-US tax resident

- Whether your home country has a tax treaty with the US.

- What type of income you are receiving

This is exactly where the W8 and W9 forms come in.

Use our quick IRS Form Finder below to see which tax form best suits your situation.

Which IRS Tax Form Do You Need?

Answer a few quick questions and we’ll point you to the right form

W8 Vs. W9 – What Is the Difference and Which One You Need?

The quick way to understand the difference between W8 and W9 is this:

- W9 is for US tax residents (individuals and entities)

- W8 is for non-US tax residents (individuals and entities)

When you submit one of these forms to a payer, you are certifying your tax residency status so they know how much – if any – withholding tax to apply to your payments.

One very important thing to understand upfront: W8 and W9 forms are not filed with the IRS. You do not submit them to the IRS directly. Instead, you submit them to each individual payer – Stripe, Shopify, Amazon, a US client company, a US SaaS platform, and so on.

This also means you will require to fill out multiple forms if you receive income from multiple US payers. And if your circumstances change – for example, you change your country of residence, your business structure changes, or your US tax status changes – you will require to submit updated forms to your payers.

Who Is a “US Tax Resident”?

This is a question that confuses many people, so it is worth spending a moment on it. Being a US tax resident does not necessarily mean you live in the United States. Under US tax law, the following individuals are considered US tax residents regardless of where they physically live:

- US citizens – even if they live permanently in another country

- US green card holders (lawful permanent residents) – again, regardless of where they currently reside

In addition, foreign nationals physically present in the United States may also be considered US tax residents if they meet the Substantial Presence Test. This test calculates whether you have been physically present in the US for enough days over a rolling three-year period to be treated as a tax resident. This can apply even to people on tourist visas, so if you spend significant time in the US, it is worth checking whether you meet this threshold.

If you do not fall into any of the above categories, you are a non-US tax resident and will need to file a W8 form.

Section 1: Guide for US Tax Resident Individuals (Form W9)

If you are a US citizen, green card holder, or foreign national who qualifies as a US tax resident under the Substantial Presence Test, you need to file Form W9.

What Is Form W9?

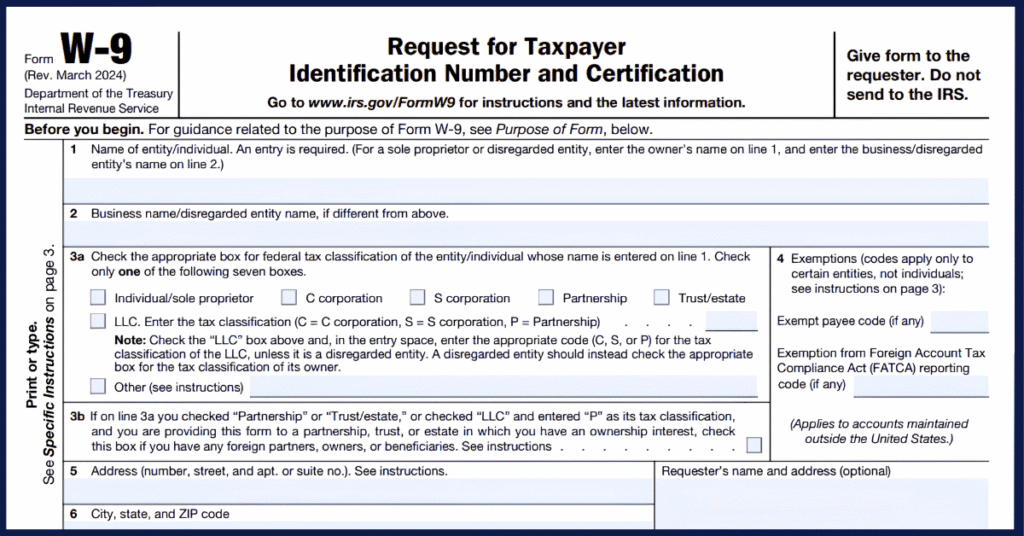

Form W9 is a single-page form titled “Request for Taxpayer Identification Number and Certification.” It tells the payer your name, address, and US taxpayer identification number (TIN), and certifies that you are a US taxpayer.

How to Fill Out Form W9 as an Individual

Line 1 – Name: Enter your full legal name as it appears on your tax return. This should be your personal name, not a business name.

Line 2 – Business name/DBA: If you operate under a “doing business as” (DBA) name that is different from your legal name, enter it here. Otherwise, leave it blank.

Line 3 — Federal tax classification: Tick the box labeled Individual/sole proprietor or single-member LLC if you are filling this out as an individual or as the owner of a single-member LLC.

Line 4 – Exemptions: Most individuals leave this blank. Exemptions apply mainly to certain corporations and specific entities exempt from backup withholding.

Lines 5 and 6 – Address: Enter your full current mailing address, including street address, city, state, and ZIP code.

Part I – Taxpayer Identification Number: Enter your Social Security Number (SSN) in the box provided. If you do not have an SSN, you may enter your Employer Identification Number (EIN) instead, though SSN is the standard for individuals.

Part II – Certification: Read the certification statements, then sign and date the form.

That is it – the W9 for individuals is straightforward and should only take a few minutes to complete.

Section 2: Guide for Non-US Resident Individuals (Form W-8BEN)

If you are an individual who is not a US citizen, not a green card holder, and does not meet the Substantial Presence Test, you need to file Form W-8BEN. The “BEN” stands for “Beneficial Owner.”

What Is Form W-8BEN?

Form W-8BEN is a Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting. By submitting this form, you are certifying to the payer that you are not a US tax resident, which affects how much withholding tax they need to apply to your payments.

The standard US withholding tax rate for non-residents is 30%. However, if your home country has a tax treaty with the United States, that rate may be significantly reduced – sometimes to 0%. The W-8BEN is also used to claim these treaty benefits.

How to Fill Out Form W-8BEN (Without Tax Treaty Claim)

If you are not claiming tax treaty benefits, you only need to complete Part I of the form:

Box 1 – Name of individual who is the beneficial owner: Enter your full legal name.

Box 2 – Country of citizenship: Enter the country of which you are a citizen.

Box 3 – Permanent residence address: Enter your full home address, including the country. This must be a physical address, not a P.O. box. This address determines your country of tax residence.

Box 4 – Mailing address (if different): Enter a mailing address here only if it is different from your permanent residence address.

Box 5 – U.S. taxpayer identification number (SSN or ITIN): Enter your SSN or ITIN if you have one. If you do not have either, leave this blank — it is not required for most non-US residents unless you are claiming treaty benefits.

Box 6a – Foreign tax identifying number: Enter the tax identification number issued by your home country (for example, your National Insurance number in the UK, your PAN in India, your SIN in Canada). If your country does not issue such numbers, tick the box in 6c instead.

Box 6b – Check if FTIN not legally required: Tick this only if your country does not require individuals to obtain a foreign tax identification number.

Box 8 – Date of birth: Enter your date of birth in MM-DD-YYYY format.

Certification box at the bottom: Tick the checkbox to certify the information is correct.

Signature and date: Sign and date the form in the signature area.

Leave all other boxes blank.

How to Fill Out Form W-8BEN (Claiming Tax Treaty Benefits)

If your home country has a tax treaty with the United States and you want to claim reduced withholding tax rates, you will also need to complete Part II of the form, in addition to everything in Part I above.

Box 9 – Country claiming treaty benefits: Enter the name of the country under whose tax treaty you are claiming benefits. This must be the same country as your country of tax residence.

Box 10 – Special rates and conditions: This is the key box. You will need to enter four pieces of information:

- The article (paragraph) of the treaty that grants the benefit you are claiming

- The withholding tax rate you are claiming under that article

- The type of income the reduced rate applies to

- A brief explanation of why you are entitled to claim the benefit

For example, if you are a UK tax resident claiming a 0% withholding rate on royalties under the US-UK tax treaty:

“United Kingdom – Article 12, Paragraph 1 – 0% – Royalties – Tax resident of the United Kingdom entitled to benefits under the US-UK Income Tax Treaty.”

You can find a full list of US tax treaties and their terms on the IRS website. Each treaty is different, so make sure you are referencing the correct article and rate for the specific type of income you are receiving.

Section 3: Guide for US Tax Resident Legal Entities (Form W9)

US-registered and US tax resident legal entities – including corporations, partnerships, and LLCs treated as corporations – use the same Form W9 as US tax resident individuals, with some differences in how it is filled out.

How to Fill Out Form W9 for a Legal Entity

Line 1 – Name: Enter the full legal registered name of your business exactly as it appears on your formation documents and IRS registrations.

Line 2 – Business name/DBA: If your business operates under a trade name or DBA that is different from its legal registered name, enter it here.

Line 3 – Federal tax classification: Tick the box that correctly describes your entity type:

- C Corporation — for a standard US corporation

- S Corporation — for a US corporation that has elected S-corp status

- Partnership — for a US partnership

- Trust/estate — for a trust or estate

- LLC — tick this and then enter the tax classification letter: C (C-corp), S (S-corp), or P (partnership). Do not tick the LLC box if you are a single-member LLC that is a disregarded entity owned by an individual — in that case, the individual owner files the form using their own information.

Line 4 – Exemptions: Certain US corporations and other entities may be exempt from backup withholding or FATCA reporting. Most small businesses leave this blank.

Lines 5 and 6 – Address: Enter your business’s address.

Part I – Taxpayer Identification Number: Enter your business’s Employer Identification Number (EIN) in the EIN box. Do not enter an SSN for a business entity.

Part II – Certification: An authorized representative should sign and date the form on behalf of the business.

Section 4: Guide for Non-US Legal Entities (Form W-8BEN-E)

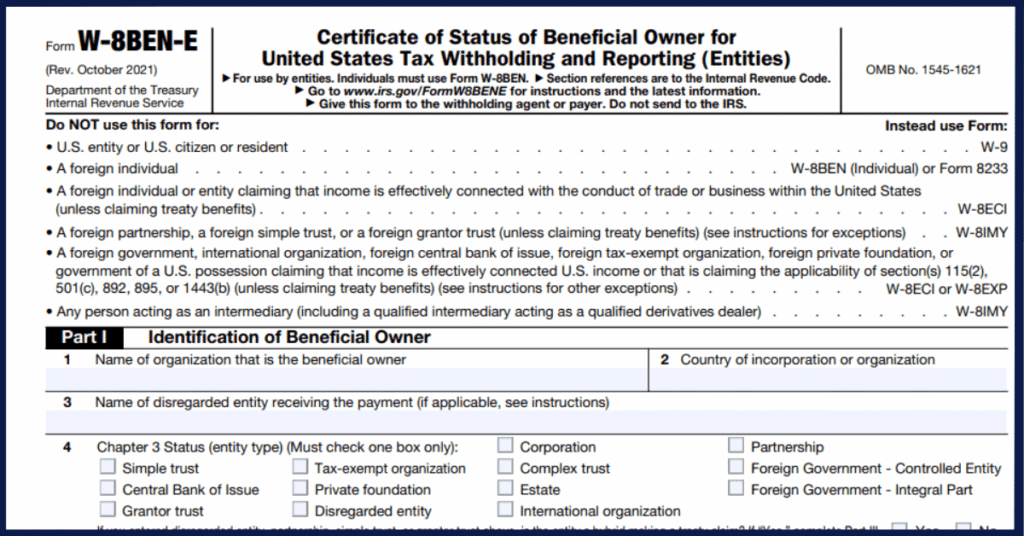

If you own a non-US company – a limited company registered in the UK, a corporation registered in Canada, a company registered in Germany, or anywhere else outside the United States — and you receive US-sourced income, you will generally need to file Form W-8BEN-E.

Form W-8BEN-E is significantly more complex than W-8BEN. It is a multi-page form with 30+ parts covering different entity classifications under FATCA (the Foreign Account Tax Compliance Act) and other US tax rules.

However, for most small to medium-sized foreign businesses, only a handful of sections are actually relevant. Here is a practical step-by-step guide for the most common scenario – a straightforward active foreign business that is not a financial institution:

How to Fill Out Form W-8BEN-E (Standard Active Foreign Business)

Box 1 – Name of organization: Enter the full legal registered name of your business.

Box 2 – Country of incorporation or organization: Enter the country where your business is legally registered.

Box 3 – Name of disregarded entity: Leave blank unless your organization is being treated as a disregarded entity under US tax rules (rare for foreign companies).

Box 4 – Chapter 3 Status: Tick the box that best describes your entity. For most foreign companies, this will be Corporation or Partnership. If your company is a simple operating company, Corporation is typically the right choice. If unsure, consult a tax advisor.

Box 5 – Chapter 4 (FATCA) Status: This is the FATCA classification box. For most ordinary foreign operating businesses:

- Tick Active NFFE if your business is an active operating business (most of its income comes from active business operations, not passive investments). An Active NFFE means “Active Non-Financial Foreign Entity.”

- Tick Passive NFFE if your business is primarily a holding company or earns mostly passive income (interest, dividends, royalties, etc.). A Passive NFFE means “Passive Non-Financial Foreign Entity.”

Boxes 6 and 7 – Permanent residence and mailing address: Enter your business’s registered address and mailing address.

Box 8 – U.S. taxpayer identification number: Enter your EIN if your business has been assigned one by the IRS. If not, leave blank.

Box 9b – Foreign tax identifying number: Enter the tax identification number issued to your business by your home country (such as your UTR in the UK, your ABN in Australia, or your BN in Canada).

Box 9c: Tick this box if your jurisdiction does not issue tax identification numbers to entities.

Part XXV – Active NFFE: If you ticked Active NFFE in Box 5, go to Part XXV and tick the certification box confirming that your entity qualifies as an Active NFFE.

Part XXVI – Passive NFFE: If you ticked Passive NFFE in Box 5, go to Part XXVI and tick the certification box. You will also need to answer the question at the bottom of Part XXVI about whether your entity has any substantial US owners, and provide details if applicable.

Part XXX – Certification: An authorized representative of the business should sign and date the form here, along with their printed name and title.

Claiming Tax Treaty Benefits for Foreign Entities

If your business is located in a country that has a tax treaty with the United States, and you want to claim reduced withholding tax rates on the income your business receives, you will also need to complete Part III of Form W-8BEN-E.

The process is the same as described for individuals in the W-8BEN section above: enter the country, the relevant treaty article and paragraph, the rate you are claiming, the type of income, and a brief explanation. Make sure you are referencing the correct tax treaty and article for your specific situation.

Section 5: US LLC – The Special Rules You Need to Know

This is the section most relevant to GenZone clients, because it addresses the specific rules that apply to US LLCs – especially single-member LLCs owned by foreign individuals or foreign companies.

What Is a “Disregarded Entity”?

Under US tax law, a US LLC with a single owner is typically treated as what the IRS calls a “disregarded entity.” This is an important concept. It means the LLC is legally disregarded for US tax purposes – it is treated as if it does not separately exist from its owner. As a result, the LLC itself does not file taxes or submit tax residency forms on its own behalf. Instead, everything flows through to the owner.

The practical implication for W8/W9 purposes is significant: if you own a single-member US LLC and a payer asks for a W8 or W9 form, you must file the form using your own personal or corporate details – not your LLC’s details.

This catches many foreign LLC owners off guard. They receive a W8/W9 request, assume they should submit the form using the LLC’s name and details, and end up submitting the wrong information. Do not make this mistake.

Who Files What for a Disregarded LLC?

The correct form to file depends on who the owner of the LLC is and what their tax status is:

Scenario 1: The LLC owner is a non-US resident individual: File Form W-8BEN using your own personal details (not the LLC’s details). In Box 3 of the W-8BEN, enter your personal address. If you have a US EIN for your LLC, you may still enter it in the FTIN section, but the form should be in your name.

Scenario 2: The LLC owner is a non-US legal entity (foreign company): File Form W-8BEN-E using the details of the foreign parent company (not the LLC’s details). Enter the foreign parent company’s name, country of registration, and tax ID.

Scenario 3: The LLC owner is a US tax resident individual: File Form W9 using your own personal details.

Scenario 4: The LLC owner is a US legal entity: File Form W9 using the details of the US parent entity.

In short: when dealing with a disregarded entity LLC, always look through the LLC to the owner, and file based on the owner’s details and tax status.

What About Multi-Member LLCs?

A US LLC with multiple members is treated differently. Multi-member LLCs are generally treated as partnerships for US tax purposes. In this case, the LLC itself would typically file a Form W-8IMY (see Section 6 below) if it receives US withholdable income, with each member filing their own individual form as well.

Common Mistakes to Avoid

- Filing in the LLC’s name when you should file in the owner’s name. A disregarded entity does not exist for tax purposes – file using the owner’s details.

- Using an LLC’s EIN as the TIN when a personal SSN or ITIN is required. For W-8BEN purposes, your personal identifying information is what matters.

- Submitting a W9 when you should submit a W8 because your LLC is a US entity. Remember, the LLC being US-registered does not make you a US tax resident if you are a foreign individual owner.

- Forgetting to re-file when circumstances change. If you take on a second member, the LLC may no longer be a disregarded entity and different rules apply.

Section 6: Foreign Partnerships – UK LLP, BC LLP, ON LP, and Similar Entities

Foreign partnerships are a common structure for international entrepreneurs, particularly those who use UK Limited Liability Partnerships (UK LLPs), British Columbia Limited Partnerships (BC LLPs), or Ontario Limited Partnerships (ON LPs). These entities have unique W8 filing requirements.

Standard Case: Documenting Tax Residency

In most standard situations, a foreign partnership that needs to document its tax residency status or claim tax treaty benefits will file Form W-8BEN-E, following the instructions in Section 4 of this guide.

However, foreign partnerships need to be careful about one important distinction.

Special Case: Receiving US Withholdable Income

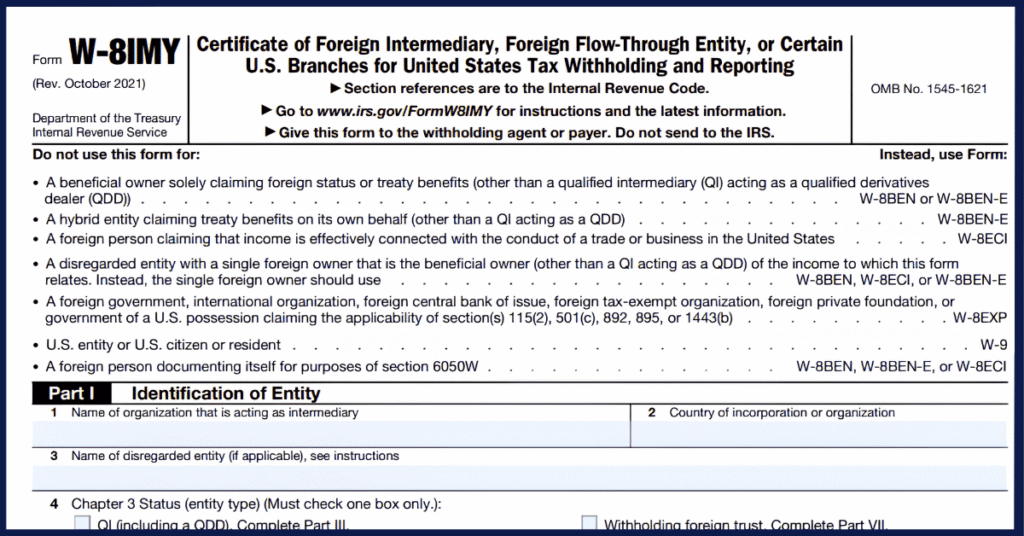

If a foreign partnership directly receives income that is subject to US withholding tax, the situation becomes more complex. In this case, the partnership itself cannot simply submit a W-8BEN-E. Instead:

- The partnership must file Form W-8IMY. This form identifies the partnership as an intermediary – it is passing income through to its partners – and certifies the partnership’s status to the US payer.

- Each individual partner must also file their own appropriate form – W9 (if a US tax resident), W-8BEN (if a non-US resident individual), or W-8BEN-E (if a non-US entity), depending on their personal status.

- A withholding statement must be attached to the W-8IMY. This statement allocates the income among the partners and tells the payer how much withholding to apply to each partner’s share of the income.

This process is considerably more involved than a simple single-owner LLC scenario, and if you are involved in a foreign partnership receiving US withholdable income, we strongly recommend consulting a qualified US tax advisor.

Section 7: Tax Treaties – Reducing Your Withholding Rate

One of the most valuable aspects of the W8 form system is the ability to claim reduced withholding tax rates under tax treaties. The standard US withholding rate for non-residents is 30%, but many countries have negotiated significantly lower rates – sometimes 0% – for specific types of income.

How Tax Treaties Work

The United States has tax treaties with dozens of countries around the world. Each treaty is different, but they generally reduce withholding tax rates on:

- Royalties (payments for intellectual property, copyrights, patents, trademarks, etc.)

- Dividends (distributions from US corporations)

- Interest (payments from US financial instruments)

- Business profits (in some limited circumstances)

The specific reduced rate depends on the type of income and the treaty article that applies.

Common Examples

Here are a few examples of how treaty claims work in practice:

UK resident receiving US royalties: The US-UK tax treaty typically provides a 0% withholding rate on royalties. In Box 10 of W-8BEN, you would enter: United Kingdom – Article 12 – 0% – Royalties – Tax resident of the United Kingdom.

Canadian resident receiving US dividends: The US-Canada treaty typically provides a reduced 15% rate on dividends (vs. the standard 30%). You would enter the relevant article number and rate in Box 10.

Australian resident receiving US interest: The US-Australia treaty typically provides a 10% rate on interest income from certain sources.

How to Find the Right Treaty Information

The IRS publishes all current US tax treaties on its official website (you can find it here). Always check the actual treaty document to confirm the applicable article number and rate for the specific type of income you are receiving, as treaty terms can change and the details vary.

Section 9: Summary Cheat Sheet

| Situation | Correct Form |

|---|---|

| US citizen or green card holder (individual) | W9 |

| Foreign national resident in US (Substantial Presence Test met) | W9 |

| Non-US resident individual | W-8BEN |

| US corporation, S-corp, or partnership | W9 |

| Non-US company or foreign legal entity | W-8BEN-E |

| Single-member US LLC, foreign individual owner | W-8BEN (owner’s details) |

| Single-member US LLC, foreign company owner | W-8BEN-E (owner’s details) |

| Single-member US LLC, US individual owner | W9 (owner’s details) |

| Foreign partnership (standard) | W-8BEN-E |

| Foreign partnership receiving US withholdable income | W-8IMY + partner forms |

How GenZone Can Help

Navigating US tax forms as a foreign business owner can be complicated, especially when you factor in disregarded entity rules, FATCA classifications, and tax treaty claims.

It is actually one of those areas where we see even seasoned entrepreneurs get tripped up – not because they are careless, but because the rules are genuinely not straightforward for non-US owners. At GenZone, we help international entrepreneurs form and manage US LLCs with confidence.

Our services include:

- US LLC formation – we handle the registration process from start to finish

- EIN obtainment – we help you get your Employer Identification Number from the IRS

- Compliance guidance – we help you understand your ongoing US compliance obligations

- Form support – we help you understand which W8 or W9 form applies to your situation

Get in touch with our team of experts in US LLC formation and tax filing, and book a free strategy call using the button below to discuss the best setup for your business.